Money can grow in different ways, and two common methods are dividends and interest. Imagine Ali invests in a company and receives a small payment every few months because the company earns profit.

At the same time, his friend Ahmed puts money in a savings account and receives extra money from the bank. Ali earns dividends, while Ahmed earns interest. This simple example explains the difference between dividends and interest in real life.

Many learners and investors often confuse these two financial terms because both provide income. However, the difference between dividends and interest is very important in business, banking, and investing.

Understanding the difference between dividends and interest helps people make smarter financial decisions.

Whether someone is a student, investor, or business owner, learning the difference between dividends and interest can improve financial knowledge and planning.

Key Difference Between Dividends and Interest

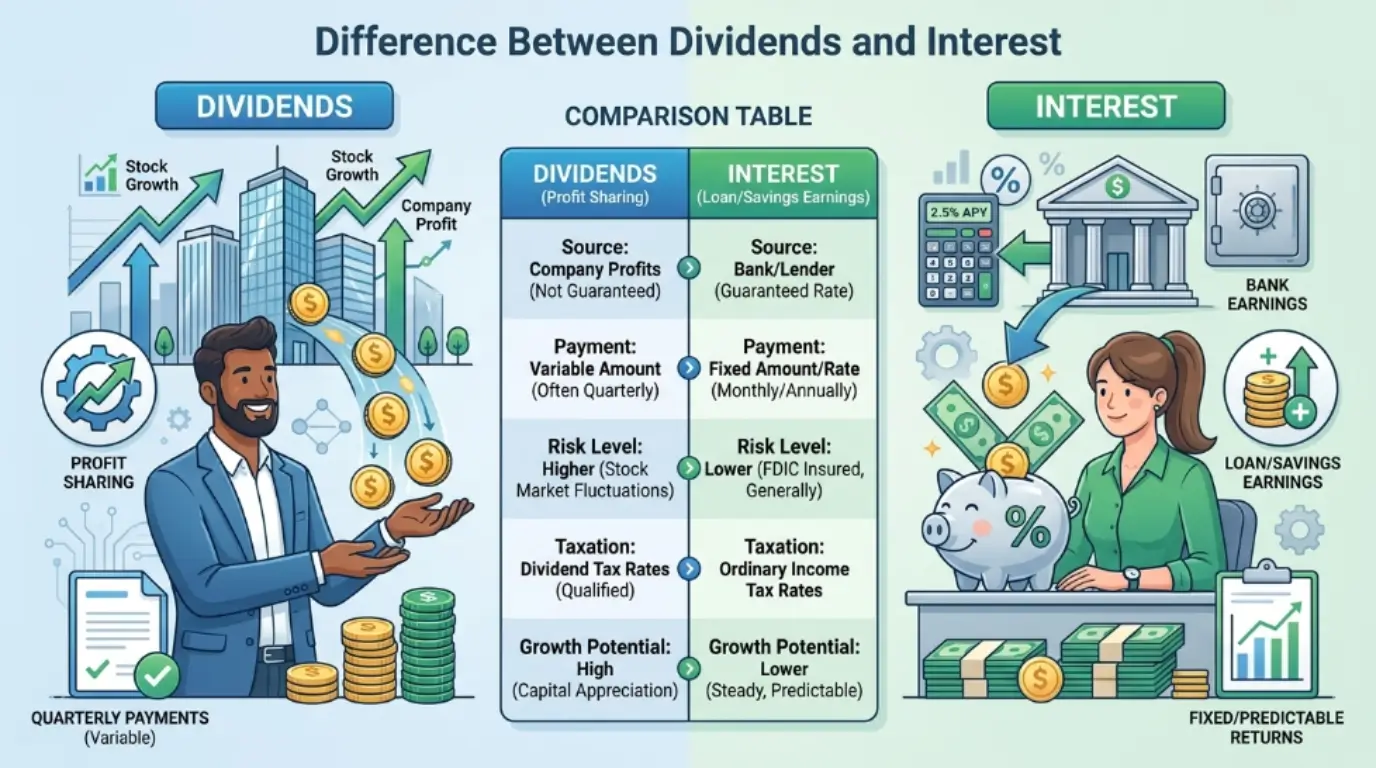

The main difference is that dividends are payments made by companies to shareholders from profits, while interest is money paid for borrowing or saving funds. Dividends depend on company performance, but interest is usually fixed by agreement.

Why Is Their Difference Important to Know?

Knowing the difference between dividends and interest is important for students, investors, and professionals. It helps people understand how businesses reward investors and how banks handle money.

In society, this knowledge supports better investment choices, financial growth, and economic awareness. Investors can decide whether they want stable income through interest or higher profit potential through dividends.

Pronunciation

- Dividends

- US: /ˈdɪv.ə.dendz/

- UK: /ˈdɪv.ɪ.dendz/

- Interest

- US: /ˈɪn.trəst/

- UK: /ˈɪn.trɪst/

Both terms may seem similar because they involve earning money, but their source, purpose, and financial meaning are very different. Let us now explore the detailed comparison.

Difference Between Dividends and Interest

1. Meaning

- Dividends: A share of company profit paid to shareholders.

- Example 1: A company gives yearly profit shares to investors.

- Example 2: Shareholders receive cash after business success.

- Interest: Money paid for borrowing or saving money.

- Example 1: A bank pays interest on savings accounts.

- Example 2: A borrower pays interest on a loan.

2. Source

- Dividends: Come from company profits.

- Example 1: Tech companies distribute yearly earnings.

- Example 2: Retail firms reward shareholders after profit growth.

- Interest: Comes from lending agreements.

- Example 1: Banks charge borrowers interest.

- Example 2: Investors earn interest from bonds.

3. Fixed or Variable

- Dividends: Usually variable.

- Example 1: A company increases dividends in a strong year.

- Example 2: Dividends may stop during losses.

- Interest: Often fixed.

- Example 1: A savings account gives 5% yearly interest.

- Example 2: Loan agreements set fixed interest rates.

4. Risk Level

- Dividends: Higher risk because profits may change.

- Example 1: Economic slowdown reduces dividends.

- Example 2: Startups may not pay dividends at all.

- Interest: Lower risk with stable returns.

- Example 1: Government bonds give secure interest.

- Example 2: Fixed deposits provide predictable income.

5. Who Receives It?

- Dividends: Shareholders receive them.

- Example 1: Investors in a company earn dividends.

- Example 2: Stock owners get yearly profit shares.

- Interest: Lenders or savers receive it.

- Example 1: Banks pay customers interest.

- Example 2: Bondholders earn interest income.

6. Purpose

- Dividends: Reward ownership in a company.

- Example 1: Shareholders benefit from company success.

- Example 2: Investors feel encouraged to keep shares.

- Interest: Compensate for using money.

- Example 1: Banks earn from lending money.

- Example 2: Borrowers pay for loan usage.

7. Tax Treatment

- Dividends: Sometimes taxed differently.

- Example 1: Qualified dividends may get lower tax rates.

- Example 2: Some countries exempt small dividends.

- Interest: Usually taxed as regular income.

- Example 1: Bank interest is taxable income.

- Example 2: Bond interest may require yearly tax filing.

8. Payment Frequency

- Dividends: Paid quarterly or yearly.

- Example 1: Companies announce quarterly dividends.

- Example 2: Some firms pay yearly bonuses to shareholders.

- Interest: Paid monthly, quarterly, or yearly.

- Example 1: Savings accounts credit monthly interest.

- Example 2: Loans require monthly interest payments.

9. Legal Obligation

- Dividends: Not legally required.

- Example 1: Companies can skip dividends in difficult times.

- Example 2: Boards decide dividend payments.

- Interest: Legally required by contract.

- Example 1: Borrowers must pay loan interest.

- Example 2: Bonds promise fixed interest payments.

10. Financial Nature

- Dividends: Equity income.

- Example 1: Linked with stock ownership.

- Example 2: Depends on company performance.

- Interest: Debt income.

- Example 1: Connected with loans and bonds.

- Example 2: Earned through lending money.

Nature and Behaviour of Both

Dividends are connected with business profits and company growth. Their behaviour changes with market performance. If a company performs well, dividends may rise.

Interest is more stable and predictable. It depends on financial agreements between lenders and borrowers. Interest rates can change with economic policies, but payments are usually regular.

Why Are People Confused About Their Use?

People confuse dividends and interest because both provide income from money. They also appear in banking and investment discussions together. Another reason is that both can create passive income. However, dividends come from ownership, while interest comes from lending.

Difference and Similarity Table

| Feature | Dividends | Interest | Similarity |

| Source | Company profits | Borrowed money | Both provide income |

| Receiver | Shareholders | Lenders/Savers | Both reward investors |

| Risk | Higher | Lower | Both involve financial return |

| Nature | Equity-based | Debt-based | Both relate to money growth |

| Payment | Variable | Usually fixed | Both can be periodic |

Which Is Better in Different Situations?

Dividends are better for people who want long-term investment growth and possible higher returns. Investors who believe in company success may choose dividend-paying stocks. Dividends can also increase over time if the company grows.

Interest is better for people who want stable and predictable income. Retired individuals or low-risk investors often prefer savings accounts, bonds, or fixed deposits because interest payments are safer and more regular.

Metaphors and Similes

- “Dividends are like fruits growing from a healthy tree.”

- “Interest is like rent paid for using someone else’s money.”

- “Dividends flow like rewards from business success.”

- “Interest works like a steady river of income.”

Connotative Meaning

Dividends

- Positive: Profit, reward, growth

- Neutral: Shareholder payment

- Negative: Uncertain returns

Examples:

- “The company’s dividends made investors happy.”

- “Dividends stopped during the recession.”

Interest

- Positive: Stability, safety

- Neutral: Lending charge

- Negative: Debt burden

Examples:

- “Interest from savings helped her monthly expenses.”

- “High loan interest caused financial stress.”

Idioms and Proverbs Related to the Words

- “Money makes money.”

- Example: Smart investments in dividends and interest can grow wealth.

- “A penny saved is a penny earned.”

- Example: Saving money in an interest account builds future security.

- “Reap what you sow.”

- Example: Investors receive dividends after supporting a company.

Works in Literature

Dividends

- The Intelligent Investor — Benjamin Graham (Finance, 1949)

- Security Analysis — Benjamin Graham and David Dodd (Finance, 1934)

Interest

- Interest and Prices — Knut Wicksell (Economics, 1898)

- The Theory of Interest — Irving Fisher (Economics, 1930)

Movies Related to Finance and Investment

Dividends

- Wall Street (1987, USA)

- The Wolf of Wall Street (2013, USA)

Interest

- The Big Short (2015, USA)

- Margin Call (2011, USA)

Frequently Asked Questions

1. What is the basic difference between dividends and interest?

Dividends are profit payments to shareholders, while interest is payment for borrowed money.

2. Which is safer, dividends or interest?

Interest is generally safer because it is fixed and contract-based.

3. Can a company stop paying dividends?

Yes, companies may stop dividends during financial losses.

4. Is interest taxable?

Yes, interest income is usually taxable in most countries.

5. Why do investors like dividends?

Investors like dividends because they provide regular income and show company strength.

How Both Are Useful for Surroundings

Dividends help businesses attract investors and support economic growth. They encourage people to invest in companies, which creates jobs and innovation. Interest supports banking systems and allows people to borrow money for homes, education, and businesses. Together, both play a major role in financial development and economic stability.

Final Words

The difference between dividends and interest is simple yet very important in finance and daily life.

Dividends reward people for owning shares in a company, while interest rewards people for lending or saving money.

Although both provide financial returns, their nature, risk, and purpose are different. Understanding these terms helps learners, investors, and professionals make better financial decisions.

In modern society, knowledge about dividends and interest improves money management and investment planning.

Whether someone prefers the growth potential of dividends or the stability of interest, both are valuable tools for building financial security and wealth over time.