Understanding the difference between IRA and annuity is important for anyone planning for retirement.

Imagine two coworkers, Sarah and John, who both want financial security after retirement. Sarah chooses an Individual Retirement Account (IRA) because she wants flexibility and investment control.

John prefers an annuity because he wants guaranteed income for life. Both options help people save for retirement, but they work in very different ways.

The difference between IRA and annuity often confuses beginners because both are retirement-focused financial tools.

Their structure, benefits, risks, and tax treatment are not the same. Learning the difference between IRA and annuity helps investors make better financial decisions.

Whether you are a beginner, financial learner, or retirement expert, understanding the difference between IRA and annuity can help you choose the right path toward long-term financial stability.

Key Difference Between IRA and Annuity

An IRA is a retirement savings account that allows individuals to invest in assets such as stocks, bonds, and mutual funds. An annuity is an insurance contract designed to provide a stream of income, usually during retirement.

Why Is Their Difference Important to Know?

Knowing the distinction between an IRA and an annuity helps people select financial products that match their goals.

Investors seeking growth may prefer IRAs, while retirees seeking predictable income may choose annuities.

Financial advisors, students, and retirement planners benefit from understanding these differences because retirement planning affects individuals, families, businesses, and society as a whole.

Pronunciation

IRA

- US: /ˌaɪ.ɑːrˈeɪ/

- UK: /ˌaɪ.ɑːˈreɪ/

Annuity

- US: /əˈnuː.ə.ti/

- UK: /əˈnjuː.ə.ti/

Now that we understand the basics, let’s explore the detailed difference between IRA and annuity.

Difference Between IRA and Annuity

1. Definition

IRA: A tax-advantaged retirement savings account.

Examples:

- A teacher contributes money to a Roth IRA.

- An engineer invests through a Traditional IRA.

Annuity: An insurance product providing future income.

Examples:

- A retiree buys a lifetime annuity.

- A worker purchases a deferred annuity.

2. Purpose

IRA: Focuses on wealth accumulation.

Examples:

- Saving for retirement growth.

- Building long-term investment assets.

Annuity: Focuses on income generation.

Examples:

- Receiving monthly retirement payments.

- Ensuring lifetime financial support.

3. Ownership

IRA: Owned and managed by the account holder.

Examples:

- An individual chooses investments.

- An investor changes asset allocation.

Annuity: Issued and managed by an insurance company.

Examples:

- The insurer guarantees payments.

- The company manages investment risk.

4. Investment Options

IRA: Offers broad investment choices.

Examples:

- Stocks and ETFs.

- Mutual funds and bonds.

Annuity: Limited to insurer-provided options.

Examples:

- Fixed annuity accounts.

- Variable annuity portfolios.

5. Income Guarantee

IRA: No guaranteed income.

Examples:

- Market gains may increase value.

- Market losses may reduce value.

Annuity: Often guarantees income.

Examples:

- Fixed monthly payouts.

- Lifetime income contracts.

6. Risk Level

IRA: Higher market risk.

Examples:

- Stock market downturns.

- Investment volatility.

Annuity: Generally lower income risk.

Examples:

- Guaranteed payment schedules.

- Fixed-rate contracts.

7. Fees

IRA: Usually lower fees.

Examples:

- Low-cost index funds.

- Discount brokerage accounts.

Annuity: Often higher fees.

Examples:

- Mortality charges.

- Administrative fees.

8. Tax Treatment

IRA: Tax benefits depend on account type.

Examples:

- Traditional IRA tax deductions.

- Roth IRA tax-free withdrawals.

Annuity: Earnings grow tax-deferred.

Examples:

- Taxes delayed until withdrawal.

- Deferred income accumulation.

9. Liquidity

IRA: More flexible access.

Examples:

- Investment changes anytime.

- Easier asset transfers.

Annuity: Less liquid.

Examples:

- Surrender charges.

- Withdrawal penalties.

10. Retirement Income

IRA: Income depends on savings and withdrawals.

Examples:

- Self-managed distributions.

- Flexible withdrawal amounts.

Annuity: Provides structured income.

Examples:

- Monthly payments.

- Lifetime income streams.

Nature and Behavior of IRA and Annuity

An IRA behaves like an investment vehicle designed for growth and flexibility. Its value changes according to market performance and investment choices.

An annuity behaves like an insurance-based income solution. Its primary purpose is to provide predictable and reliable retirement income over time.

Why Are People Confused About Their Use?

People often confuse IRAs and annuities because both are associated with retirement planning and tax advantages. Additionally, annuities can sometimes be held inside IRAs, making the distinction less obvious. While both help prepare for retirement, one focuses on saving and investing, while the other focuses on generating income.

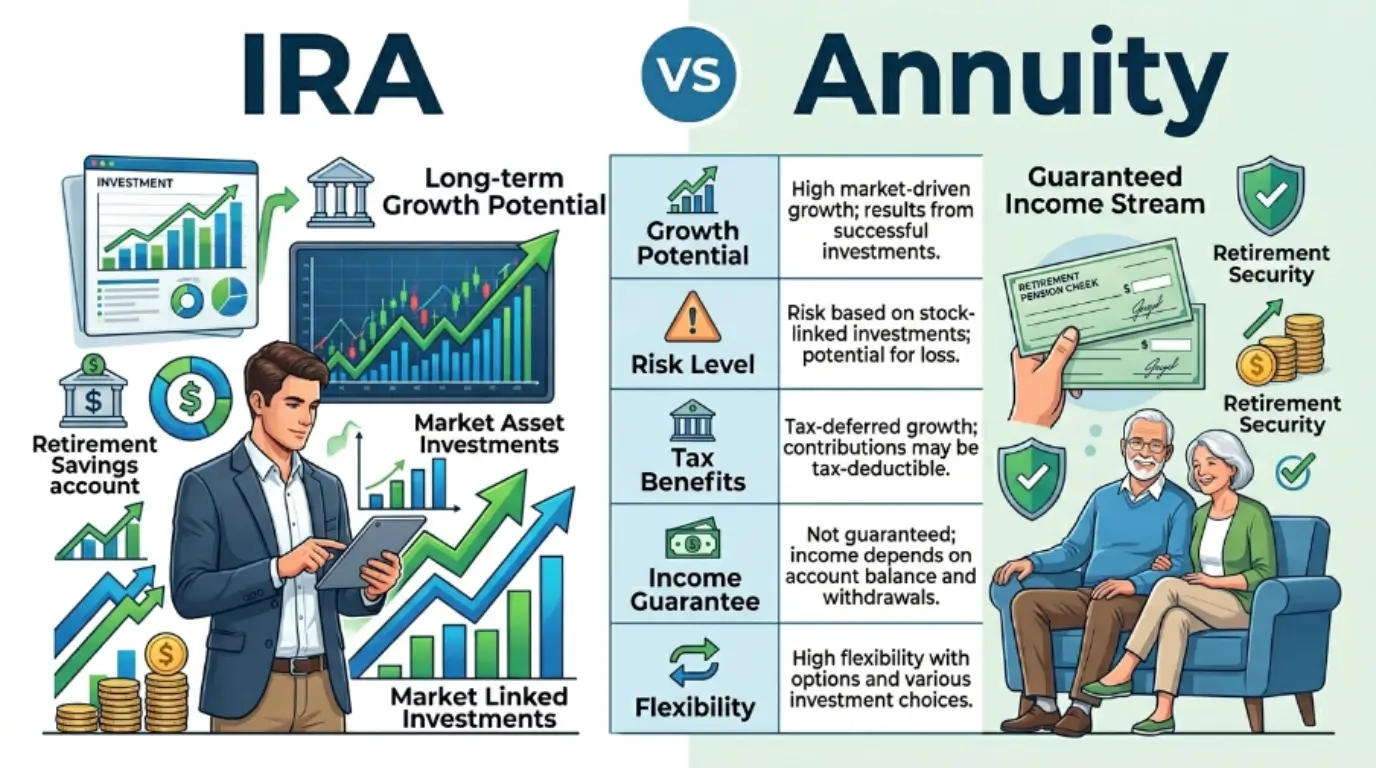

IRA vs Annuity Difference and Similarity Table

| Feature | IRA | Annuity |

| Type | Retirement account | Insurance contract |

| Main Goal | Wealth growth | Income generation |

| Investment Control | High | Limited |

| Income Guarantee | No | Usually yes |

| Tax Benefits | Yes | Yes |

| Risk Level | Market risk | Lower income risk |

| Fees | Generally lower | Generally higher |

| Liquidity | More flexible | Less flexible |

| Provider | Financial institution | Insurance company |

| Retirement Use | Saving | Income |

Similarities

| Similarity | IRA | Annuity |

| Retirement Planning | Yes | Yes |

| Tax Advantages | Yes | Yes |

| Long-Term Focus | Yes | Yes |

| Wealth Preservation | Yes | Yes |

Which Is Better and When?

An IRA is better for individuals who want investment flexibility, lower costs, and long-term growth potential.

Younger investors often benefit from IRAs because they have more time to ride out market fluctuations and accumulate wealth.

An annuity is better for retirees or people nearing retirement who prioritize predictable income.

Those who worry about outliving their savings may find annuities attractive because they can provide guaranteed payments for life.

How Are IRA and Annuity Used in Metaphors and Similes?

IRA

Metaphor:

- An IRA is a financial garden that grows over time.

Simile:

- An IRA grows like a tree planted for the future.

Annuity

Metaphor:

- An annuity is a paycheck that never retires.

Simile:

- An annuity is like a steady river flowing every month.

Connotative Meaning

IRA

Positive:

- Financial independence

- Growth

- Flexibility

Negative:

- Market uncertainty

- Investment risk

Neutral:

- Retirement savings account

Examples:

- Her IRA gave her financial confidence.

- His IRA lost value during a market decline.

Annuity

Positive:

- Security

- Stability

- Guaranteed income

Negative:

- High fees

- Limited flexibility

Neutral:

- Insurance-based retirement product

Examples:

- The annuity provided peace of mind.

- The annuity restricted quick access to funds.

Idioms and Proverbs Related to Retirement Planning

- Don’t put all your eggs in one basket.

- Save for a rainy day.

- A penny saved is a penny earned.

- Make hay while the sun shines.

- Look before you leap.

Examples:

- Investing only in one IRA violates the idea of not putting all your eggs in one basket.

- Purchasing an annuity can be a way to save for a rainy day.

Works in Literature

IRA

- The Bogleheads’ Guide to Retirement Planning — Personal Finance — Taylor Larimore — 2006

- The Retirement Savings Time Bomb — Finance — Ed Slott — 2003

Annuity

- Pensionize Your Nest Egg — Retirement Finance — Moshe Milevsky — 2010

- The New Retirement Savings Time Bomb — Finance — Ed Slott — 2016

Movies Related to Retirement and Financial Planning

IRA

- The Company Men (2010, USA)

- Wall Street: Money Never Sleeps (2010, USA)

Annuity

- Retirement Plan (2023, USA)

- Going in Style (2017, USA)

Frequently Asked Questions

1. What is the main difference between IRA and annuity?

An IRA is a retirement savings account, while an annuity is an insurance contract providing income.

2. Can I have both an IRA and an annuity?

Yes. Many retirees use both to balance growth and guaranteed income.

3. Which has lower fees?

IRAs generally have lower fees than annuities.

4. Which is safer?

Annuities typically offer more predictable income, while IRAs are subject to market fluctuations.

5. Which is better for retirement?

The best choice depends on whether you prioritize growth, income, flexibility, or security.

How Are Both Useful for Society?

IRAs encourage individuals to save and invest for the future, reducing dependence on government support.

Annuities provide income security for retirees, helping maintain financial stability. Together, they contribute to stronger retirement systems and improved economic well-being.

Conclusion

The difference between IRA and annuity comes down to their primary purpose. An IRA is designed to help individuals grow retirement savings through investments, while an annuity focuses on providing reliable income during retirement. Both offer valuable tax advantages and long-term financial benefits.

Choosing between them depends on personal goals, risk tolerance, and retirement needs.

Investors seeking growth and flexibility often prefer IRAs, whereas those wanting predictable income may favor annuities.

Understanding the difference between IRA and annuity allows individuals to create smarter retirement strategies and achieve greater financial confidence in the future.